En este mes de julio asistí a varios congresos para presentar nuestros últimos resultados sobre predicción de cadenas de suministro.

En este contexto a menudo nos referimos a la demanda como lo que en realidad son ventas, debido a que la demanda verdadera nunca se observa cuando se producen roturas de stock. Esta situación ejemplifica la necesidad de métodos de estimación para señales censuradas desde arriba. Desde el punto de vista de los profesionales, la mayoría de las personas en la industria utilizan el Suavizado Exponencial (ETS en inglés) para predecir las ventas. Hemos desarrollado un Tobit ETS (o TETS) para predecir señales que están censuradas desde arriba y/o desde abajo. Hemos hecho las cuentas y hemos implementado la solución en un paquete llamado UComp, que está disponible en CRAN para R, en GitHub para MATLAB/Octave (https://github.com/djpedregal/UComp) y en PyPI para Python.

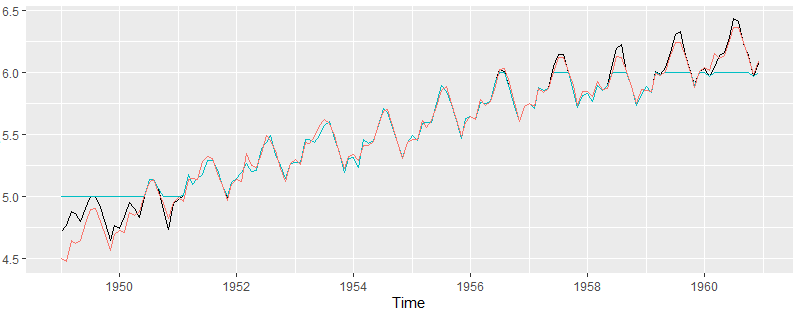

La siguiente figura muestra un caso extremo en el que los datos de AirPassengers de EE.UU. están artificialmente censurados tanto desde abajo como desde arriba. La línea negra representa los datos originales (‘demanda verdadera’), la línea azul es la misma información censurada artificialmente desde abajo y desde arriba, que es la información con la que el modelo tiene que estimar las predicciones, y la línea roja es el ajuste del modelo TETS. En otras palabras, dado solo la información restringida en azul, el modelo TETS logra estimar el ajuste en rojo más allá de los límites impuestos por las restricciones de los datos.